Section 44ADA Presumptive Taxation for Professionals – Complete Guide

If you are a professional searching for Section 44ADA details or an income tax consultant near me, this guide will help you understand everything clearly. Many professionals in Ghaziabad, Noida, and Delhi NCR struggle with maintaining books, calculating expenses, and complying with audit rules.

Section 44ADA simplifies taxation by allowing eligible professionals to declare income on a presumptive basis. However, there are important conditions, limits, and compliance rules that must be followed carefully.

✅ Latest Update

As per Finance Act, 2023, the turnover limit under Section 44ADA has been extended from ₹50 lakh to ₹75 lakh, but only when cash receipts do not exceed 5% of total receipts.

💡 Practical Explanation (Easy Understanding)

Who can use Section 44ADA?

|

Category Need help with this? Talk to AMIT SIDDHI AND ASSOCIATES → |

Eligible? |

|

Doctor, CA, Lawyer |

✅ Yes Need help with this? Talk to AMIT SIDDHI AND ASSOCIATES → |

|

Freelancer (technical consultancy) |

✅ Yes |

|

Trader/Shopkeeper |

❌ No |

Example

Suppose a consultant in Indirapuram (201014) earns ₹40 lakh:

· Under normal taxation → Actual profit calculation required

· Under 44ADA → Income = 50% = ₹20 lakh

No need to maintain detailed books.

When ₹75 lakh limit applies

|

Condition |

Limit |

|

Cash receipts ≤ 5% |

₹75 lakh |

|

Cash receipts > 5% |

₹50 lakh |

📋 Step-by-Step Compliance Process

1. Check eligibility (profession + residency)

2. Calculate total gross receipts

3. Verify cash receipts percentage

4. Declare 50% income (or higher)

5. Pay 100% advance tax by 15 March

6. File ITR-4 (if eligible)

7. Avoid audit by following presumptive rules

📚 Legal Reference

Section: Section 44ADA; Section 44AA; Section 44AB

Rule: No separate rule creating a “Form 44ADA” was found in the official sources checked.

Notification/Circular: Finance Act, 2023 amendments reflected in the updated section text; no separate official circular was needed for the core threshold update in the sources reviewed.

Official Source Links:

https://www.incometax.gov.in/iec/foportal/help/e-filing-itr4-form-sugam-faq

https://www.incometaxindia.gov.in/w/section-44ab-37

https://www.incometax.gov.in/iec/foportal/sites/default/files/2026-04/Notification%20No.45_2026.pdf

🔎 Legal Position

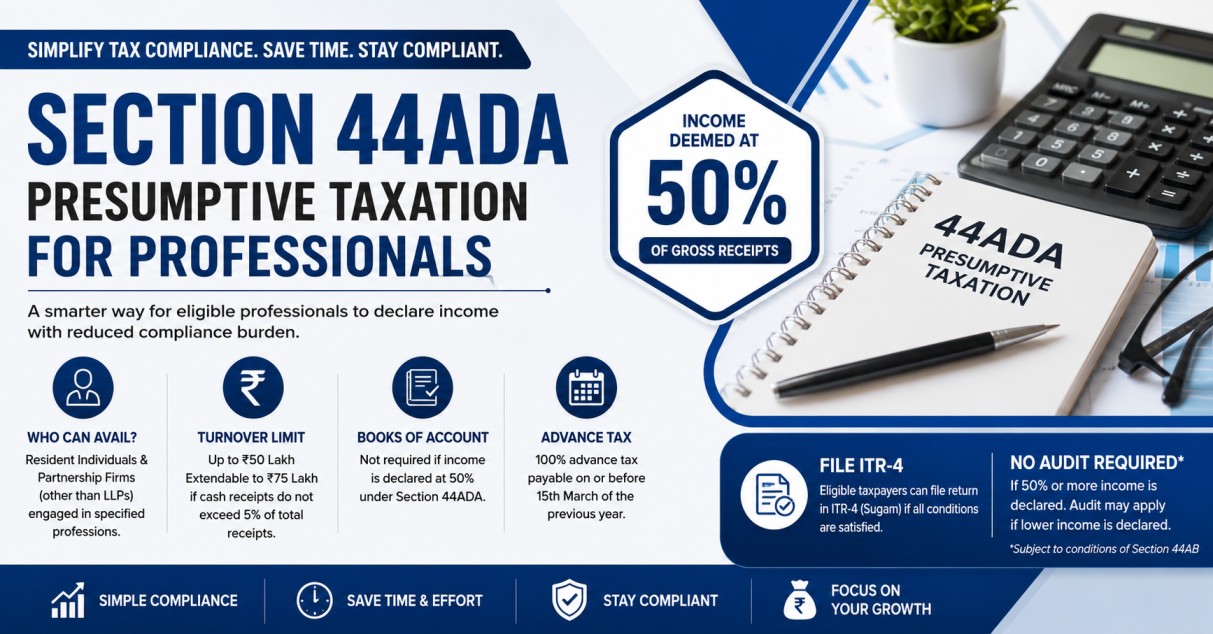

Section 44ADA applies to resident individuals and partnership firms other than LLPs engaged in specified professions, with gross receipts up to Rs. 50 lakh, extendable to Rs. 75 lakh where cash receipts do not exceed 5% of total receipts. Under the official FAQ, advance tax at 100% is payable by 15 March, and books of account are not required for the specified profession if income is declared at 50% under 44ADA.

Section 44ADA of the Income-tax Act is a presumptive taxation provision designed to simplify compliance for eligible professionals. It allows certain resident taxpayers, specifically individuals and partnership firms other than LLPs, to declare income at a fixed percentage of gross receipts instead of computing actual profits by maintaining detailed books in the ordinary way. The main purpose is to reduce compliance burden for small professionals while still ensuring a clear tax base.

The official Income Tax Department FAQ confirms that 44ADA applies to a resident person engaged in a specified profession covered under Section 44AA(1). These professions include legal, medical, engineering, architectural, accountancy, technical consultancy, interior decoration, and any other profession notified by the CBDT. This means the scheme is not open to every business or every type of self-employed activity; it is limited to the professions specifically covered by law.

Under the statutory rule, income under 44ADA is deemed to be 50% of gross receipts, unless the taxpayer voluntarily declares a higher amount. This makes the scheme attractive for professionals with relatively low actual expenses or for those who want to avoid maintaining detailed expense records. The key point is that the 50% figure is a deeming rule, not a mandatory tax rate separate from the normal slab system. The income so computed is then taxed according to the assessee’s applicable slab rates.

A major feature of the scheme is the threshold limit. The base limit is gross receipts up to Rs. 50 lakh in a previous year. However, where the amount or aggregate of amounts received in cash does not exceed 5% of total gross receipts, the limit is extended to Rs. 75 lakh. This higher threshold was inserted by the Finance Act, 2023 and is reflected in the current official text. The image is correct to mention the Rs. 75 lakh concept, but that condition must be stated carefully, because it is not a blanket threshold for everyone.

Another important compliance point is books of account. The official FAQ states that if a professional opts for presumptive taxation under Section 44ADA and declares income at 50% of gross receipts, the maintenance requirement under Section 44AA does not apply to that specified profession. This is one of the main advantages of the scheme. But the relaxation is not absolute: if the taxpayer claims lower profits than the presumptive amount and total income exceeds the basic exemption threshold, books must be maintained and audit requirements under Section 44AB can arise.

Advance tax is also relevant. The Income Tax Department FAQ says that anyone opting for 44ADA is liable to pay 100% of advance tax on or before 15 March of the previous year. Failure to do so can trigger interest under Sections 234B and 234C. This is often missed in social media graphics, yet it is a core compliance item for professionals using presumptive taxation.

The image’s overall theme is therefore partly correct but simplified in a way that can mislead. It is accurate that 44ADA is a presumptive taxation scheme for professionals and that it eases book-keeping requirements. It is also accurate that advance tax is due by 15 March and that the 50% presumptive rate is central to the scheme. But any post or infographic should clearly state the eligibility, the cash-receipt condition for the Rs. 75 lakh threshold, and the audit consequence if income is declared lower than the presumptive amount.

For practical filing, taxpayers who opt for presumptive taxation commonly use ITR-4 if otherwise eligible. The Income Tax Department’s ITR-4 FAQ states that ITR-4 can be filed by eligible resident individuals, HUFs, and firms other than LLPs having presumptive income under Sections 44AD, 44ADA, or 44AE, subject to the prescribed conditions. So, the return form is ITR-4 in many cases, but that is not the same thing as a separate legal “Form 44ADA.”

In short, Section 44ADA is real and useful, but it should be described precisely. The scheme is for eligible resident professionals, the presumptive income is 50% of gross receipts, the limit is generally Rs. 50 lakh but can extend to Rs. 75 lakh if cash receipts stay within the statutory cap, books are not required when the presumptive method is followed, and advance tax must still be paid on time. Any claim that turns this into a special standalone filing form is not supported by the official sources reviewed.

❓ Frequently Asked Questions (FAQ)

1. Is there a Form 44ADA?

No, there is no separate form. Taxpayers usually file ITR-4.

2. Can I declare income less than 50%?

Yes, but then:

· Books must be maintained

· Audit may apply under Section 44AB

3. Is audit required under 44ADA?

Not if you declare 50% or more income.

4. When is advance tax due?

100% advance tax must be paid by 15 March.

5. Can freelancers use Section 44ADA?

Yes, if they fall under specified professions like technical consultancy.

🧾 Conclusion

Section 44ADA is one of the most beneficial provisions for professionals who want to simplify taxation and reduce compliance burden. However, incorrect understanding—especially about limits, audit rules, or advance tax—can lead to penalties.

If you are searching for a tax consultant near me, income tax services near me, or GST consultant near me in Ghaziabad, Vaishali (201019), or Noida, proper guidance can help you choose the best tax strategy.

For expert guidance on this topic, contact your tax professional today.

⚠️ Disclaimer

This content is for educational and knowledge purposes only. For verification and applicability to your case, please consult your tax professional.

Have Questions? We're Here to Help

Get expert advice from AMIT SIDDHI AND ASSOCIATES. Reach out to discuss your requirements.