Complete TDS/TCS Rate Chart FY 2026-27 Under Income-tax Act 2025: Codes, Rates, Thresholds & Single Challan System

The Income-tax Act, 2025 has completely restructured the TDS and TCS framework applicable from FY 2026-27. Businesses, professionals, firms, contractors, e-commerce operators and taxpayers in Noida, Ghaziabad, Delhi NCR, Vaishali (201019), Vasundhra (201012), and Indirapuram (201014) are now required to understand the new consolidated TDS/TCS structure carefully.

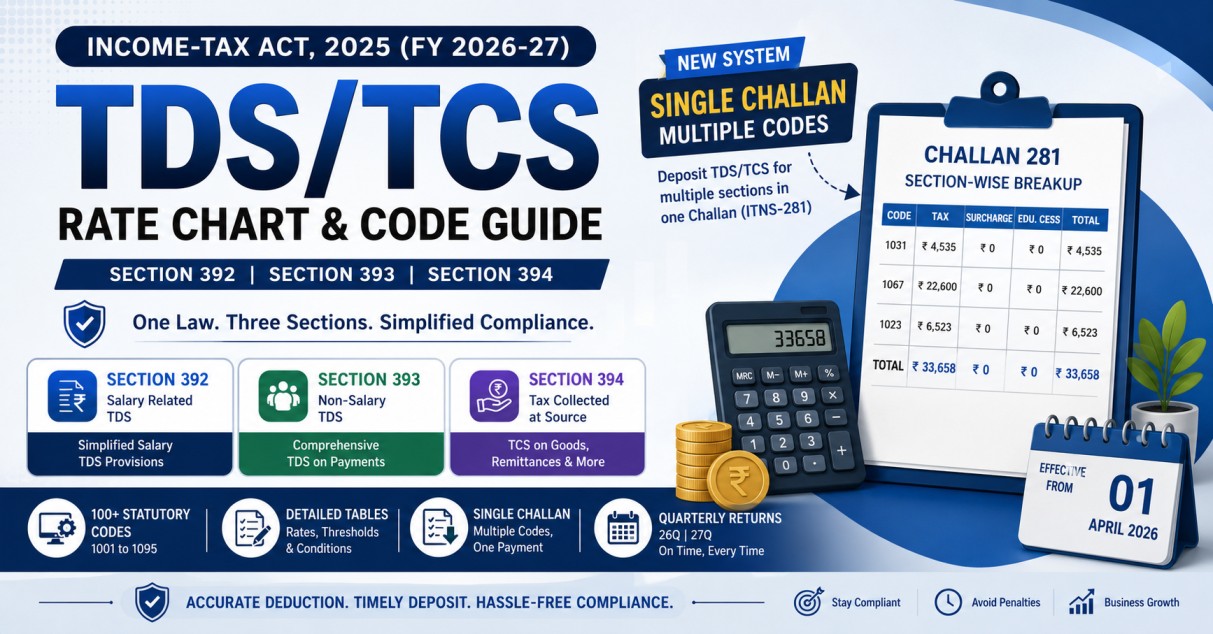

Earlier, taxpayers had to deal with dozens of separate TDS sections under the old Income-tax Act, 1961. Now, the law consolidates most TDS and TCS provisions into three major sections:

· Section 392 – Salary-related TDS

· Section 393 – Non-salary TDS

· Section 394 – Tax Collected at Source (TCS)

One of the biggest changes is the introduction of a single Challan ITNS-281 system allowing multiple TDS/TCS codes in one challan with section-wise breakup of Tax, Surcharge and Education Cess separately.

This detailed guide explains the complete TDS/TCS chart for FY 2026-27 including official codes, rates, thresholds, challan structure and compliance process.

Latest Update

As per Notification No.45/2026 and CPC(TDS) Circular No.01/CPC(TDS)/2026 effective from 01-04-2026, TDS/TCS provisions are operational under the new Income-tax Act, 2025 with standardized code-based reporting and consolidated challan structure.

The updated TDS/TCS codes range from 1001 to 1095 under the Rules, 2026 framework.

Complete TDS Rate Chart FY 2026-27 (Residents)

Section 393(1) – Key Domestic TDS Codes

|

Code |

Old Section |

Nature of Payment |

Rate |

Threshold |

|

1005 |

194D |

Insurance Commission |

2% / 10% |

₹20,000 |

|

1006 |

194H |

Commission/Brokerage |

2% |

₹20,000 |

|

1008 |

194I(a) |

Rent – Machinery |

2% |

₹50,000 per month |

|

1009 |

194I(b) |

Rent – Building |

10% |

₹50,000 per month |

|

1012 |

194IA |

Immovable Property Compensation |

10% |

₹5 Lakh |

|

1013 |

194K |

Mutual Fund Income |

10% |

₹10,000 |

|

1019 |

193 |

Interest on Securities |

10% |

₹10,000 |

|

1020 |

194A |

Interest – Senior Citizen |

10% |

₹1,00,000 |

|

1021 |

194A |

Interest – Others |

10% |

₹50,000 |

|

1023 |

194C |

Contractor – Individual/HUF |

1% / 2% |

₹30,000 / ₹1,00,000 |

|

1024 |

194C |

Contractor – Other Persons |

1% / 2% |

₹30,000 / ₹1,00,000 |

|

1026 |

194J(a) |

Technical Services |

2% |

₹50,000 |

|

1027 |

194J(b) |

Professional Services |

10% |

₹50,000 |

|

1028 |

194J |

Director Remuneration |

10% |

No limit |

|

1029 |

194 |

Dividend |

10% |

₹10,000 |

|

1030 |

194DA |

Life Insurance |

2% |

₹1 Lakh |

|

1031 |

194Q |

Purchase of Goods |

0.1% |

Above ₹50 Lakh |

|

1033 |

194R |

Business Perquisites |

10% |

₹20,000 |

|

1035 |

194O |

E-commerce Transactions |

0.1% |

₹5 Lakh |

|

1037 |

194S |

Virtual Digital Asset |

1% |

₹10,000 |

Section 393(3) – Special TDS Categories

|

Code |

Nature |

Rate |

Threshold |

|

1058 |

Lottery/Gambling Winnings |

30% |

₹10,000 |

|

1060 |

Online Gaming Winnings |

30% |

No limit |

|

1062 |

Horse Race Winnings |

30% |

₹10,000 |

|

1063 |

Lottery Commission |

2% |

₹20,000 |

|

1064 |

Cash Withdrawal – Co-op Society |

2% |

₹3 Crore |

|

1065 |

Cash Withdrawal – Others |

2% |

₹1 Crore |

|

1066 |

NSS Withdrawal |

10% |

₹2,500 |

|

1067 |

Partner Salary/Interest/Bonus |

10% |

₹20,000 |

TDS Rate Chart for Non-Residents – Section 393(2)

|

Code |

Nature |

Rate |

|

1039 |

Income for Non-resident Sportsmen |

20% |

|

1040 |

Foreign Currency Loan Interest |

5% |

|

1041 |

Rupee Bond Interest |

5% |

|

1042 |

IFSC Bond Interest |

4% |

|

1043 |

Long-term Bond Interest |

9% |

|

1045 |

Business Trust Interest |

5% |

|

1047 |

Securitisation Trust Income |

30% / 35% |

|

1050 |

Mutual Fund/Specified Company Income |

DTAA Rate |

|

1052 |

LTCG on Units |

12.5% |

|

1055 |

FII Securities Income |

20% |

|

1057 |

Other Income |

Average applicable rate |

Complete TCS Rate Chart FY 2026-27 – Section 394

|

Code |

Nature of Collection |

Rate |

|

1068 |

Alcoholic Liquor |

2% |

|

1069 |

Tendu Leaves |

2% |

|

1070 |

Timber Forest Lease |

2% |

|

1073 |

Scrap Sale |

2% |

|

1074 |

Coal/Lignite/Iron Ore |

2% |

|

1075 |

Motor Vehicle |

1% |

|

1076 |

Wrist Watch |

1% |

|

1077 |

Art Pieces |

1% |

|

1078 |

Collectibles |

1% |

|

1079 |

Yacht/Helicopter |

1% |

|

1083 |

Sports Equipment |

1% |

|

1086 |

LRS – Education/Medical |

2% |

|

1087 |

LRS – Other Purposes |

20% |

|

1088 |

Overseas Tour Package |

2% |

|

1090 |

Parking Lot Business Rights |

2% |

|

1091 |

Toll Plaza Rights |

2% |

|

1092 |

Mining/Quarry Rights |

2% |

Single Challan ITNS-281 – Major Compliance Change

The new system allows taxpayers to deposit multiple TDS/TCS liabilities through one challan.

Example Structure

|

Description |

Code |

Tax |

|

Purchase of Goods |

1031 |

₹4,535 |

|

Partner Remuneration |

1067 |

₹22,600 |

|

Contractor Payment |

1023 |

₹6,523 |

Total deposited through single challan: ₹33,658.

The challan separately displays:

· Tax

· Surcharge

· Education Cess

· Total amount

· Section-wise breakup

This system is extremely useful for accountants, tax consultants near me, GST consultant near me and businesses managing multiple TDS deductions monthly.

Practical Compliance Example

Suppose a partnership firm in Ghaziabad (201010) makes:

· Goods Purchase: ₹45,35,000

· Partner Remuneration: ₹2,26,000

· Contractor Payment: ₹3,26,150

TDS Calculation

|

Nature |

Rate |

TDS |

|

Goods Purchase |

0.1% |

₹4,535 |

|

Partner Remuneration |

10% |

₹22,600 |

|

Contractor Payment |

2% |

₹6,523 |

Total TDS = ₹33,658.

Step-by-Step TDS/TCS Compliance Process

Step 1: Identify Applicable Section

Check whether deduction falls under:

· Section 392

· Section 393

· Section 394

Step 2: Select Correct Code

Choose exact statutory code such as:

· 1023

· 1031

· 1067

· 1075

Step 3: Deduct Tax

Apply applicable threshold and rate.

Step 4: Deposit Through Challan 281

Multiple codes can be selected in single challan.

Step 5: File Quarterly Returns

· Form 26Q

· Form 27Q

· Other applicable statements

Step 6: Issue TDS Certificates

Generate:

· Form 16

· Form 16A

Important Due Dates

|

Quarter |

Deposit Due Date |

Return Due Date |

|

Q1 |

7 July |

31 July |

|

Q2 |

7 October |

31 October |

|

Q3 |

7 January |

31 January |

|

Q4 |

30 April |

31 May |

Penalties & Risks

Wrong section code or incorrect deduction may result in:

· Interest under section 201(1A)

· Late fee under section 234E

· Demand notices

· 26AS mismatch

· Disallowance of expenditure

Businesses searching for income tax consultant near me or GST services near me should ensure proper code mapping before filing returns.

Legal Reference

Section:

· Section 392 of Income-tax Act, 2025

· Section 393(1), 393(2), 393(3) of Income-tax Act, 2025

· Section 394 of Income-tax Act, 2025

· Section 397(2) of Income-tax Act, 2025

Rule:

· Income-tax Rules, 2026

· Appendix for TDS/TCS Codes and Tables

Notification / Circular:

· Notification No.45/2026

· Circular No.01/CPC(TDS)/2026

Official Source full clickable active Links:

https://www.incometaxindia.gov.in/w/tds-rates-1

https://www.incometax.gov.in/iec/foportal/sites/default/files/2026-04/Notification%20No.45_2026.pdf

https://www.incometaxindia.gov.in/documents/d/guest/notification-no-01-cpc-tds-2026-1-pdf

LEGAL POSITION

Under Income-tax Act, 2025 (effective FY 2026-27), TDS/TCS provisions consolidated into Sections 392 (salary), 393 (non-salary payments), 394 (TCS) with detailed tables specifying payment types, serial numbers, codes (1001-1095), rates, thresholds. Single challan (ITNS-281) accommodates multiple codes with section-wise tax/surcharge/cess breakup—a confirmed feature streamlining compliance.

Section 393(1) Table lists payment categories for residents including contractor payments, partner remuneration, professional fees, goods purchases and e-commerce transactions.

Section 393(2) governs payments to non-residents including royalty, dividends, interest and long-term capital gains.

Section 393(3) specifically covers special categories including winnings, partner remuneration and cash withdrawals.

Section 394 governs TCS provisions including goods, scrap, vehicles, luxury products, overseas tour packages and foreign remittances.

Single challan mandatory format displays:

· Tax

· Surcharge

· Education Cess

· Code-wise breakup

· Section-wise breakup

Mandatory applicability starts from 01-04-2026.

Descriptions in challan and return filing system must match statutory tables verbatim.

Standardized codes 1001-1095 are prescribed under Rules, 2026.

Frequently Asked Questions (FAQ)

1. Can multiple TDS sections be paid through one challan?

Yes. Under Income-tax Act 2025, single Challan ITNS-281 supports multiple codes with section-wise breakup.

2. What is Code 1067?

Code 1067 applies to partner remuneration, commission, bonus or interest under Section 393(3).

3. What is the TDS rate on purchase of goods?

Code 1031 applies at 0.1% on purchases exceeding ₹50 lakh.

4. Is the old TDS structure abolished?

The old provisions are consolidated into Sections 392, 393 and 394 from FY 2026-27.

5. What is the TCS rate on overseas tour packages?

TCS applies under Code 1088 at 2%.

6. Is PAN mandatory?

Yes. Section 397(2) requires valid PAN submission, otherwise higher TDS/TCS rates may apply.

7. Can businesses in Noida or Delhi NCR use the same challan system?

Yes. The law applies uniformly across India including Noida, Delhi, Ghaziabad and NCR regions.

Conclusion

The Income-tax Act, 2025 has significantly modernized the TDS/TCS ecosystem by introducing consolidated sections, standardized codes and single challan functionality. Businesses, professionals, firms and deductors should carefully understand the revised structure to avoid non-compliance, penalties and reconciliation issues.

Taxpayers handling contractor payments, goods purchases, professional fees, partner remuneration or overseas transactions should regularly verify applicable codes, thresholds and return filing requirements.

For expert guidance on this topic, contact your tax professional today.

Final Disclaimer

This content is for educational and knowledge purposes only. For verification and applicability to your case, please consult your tax professional.

Have Questions? We're Here to Help

Get expert advice from AMIT SIDDHI AND ASSOCIATES. Reach out to discuss your requirements.