Complete TDS & TCS Rate Chart FY 2026-27 (AY 2027-28) with Section-wise Comparison

If you are searching for the latest TDS rate chart FY 2026-27 with section comparison, you are not alone. Many taxpayers and businesses in Ghaziabad and Noida are confused due to the shift from old sections like 194C, 194J to the new structure under the Income-tax Act 2025.

Whether you are a business owner, professional, or looking for an income tax consultant near me, understanding section-wise mapping, rates, and thresholds is essential to avoid errors in TDS compliance.

✅ Latest Update

As per the verified chart updated on 08.04.2026:

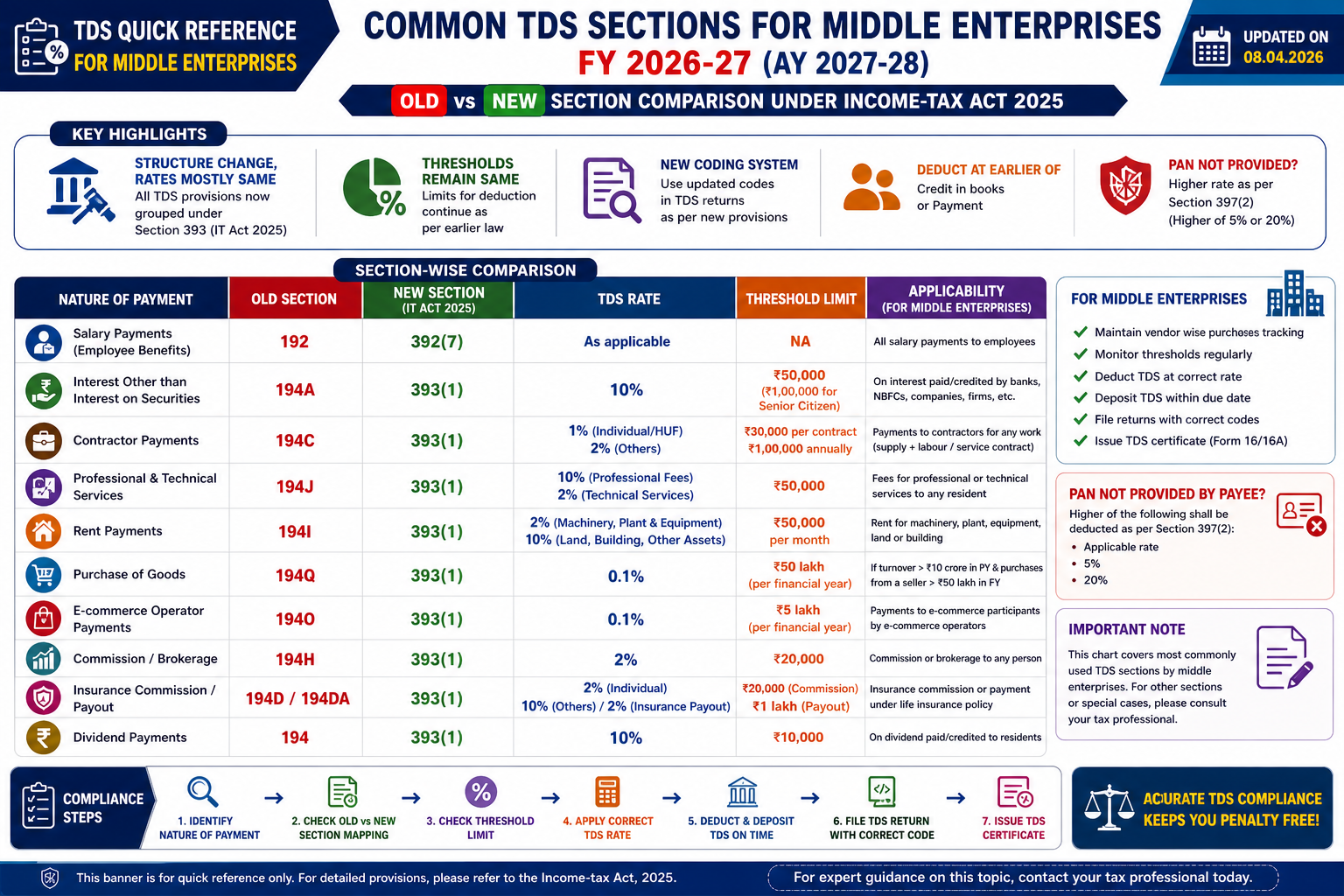

· All TDS provisions are now structured under Section 393

· TCS provisions are under Section 394

· Section-wise codes introduced for return filing

· Rates remain largely unchanged

If no further notification is issued:

➡️ No recent official update found as of today

✅ Category-wise TDS Section Comparison (Old vs New – IT Act 2025)

🔹 1. Salary & Employee Related

|

Old Section |

New Section |

Nature |

Rate |

Threshold |

|

192A |

392(7) |

EPF Withdrawal |

As applicable |

NA |

👉 No major structural change, only section renumbering.

🔹 2. Interest Income

|

Old Section |

New Section |

Nature |

Rate |

Threshold |

|

193 |

393(1) |

Interest on securities |

10% |

₹10,000 |

|

194A |

393(1) |

Interest (Senior Citizen) |

10% |

₹1,00,000 |

|

194A |

393(1) |

Interest (Others) |

10% |

₹50,000 / ₹10,000 |

🔹 3. Contract & Business Payments

|

Old Section |

New Section |

Nature |

Rate |

Threshold |

|

194C |

393(1) |

Contractor (Individual/HUF) |

1% |

₹30K / ₹1L |

|

194C |

393(1) |

Contractor (Others) |

2% |

₹30K / ₹1L |

🔹 4. Professional & Technical Services

|

Old Section |

New Section |

Nature |

Rate |

Threshold |

|

194J(b) |

393(1) |

Professional Fees |

10% |

₹50,000 |

|

194J(a) |

393(1) |

Technical Services |

2% |

₹50,000 |

|

194J |

393(1) |

Director Remuneration |

10% |

No limit |

🔹 5. Commission & Brokerage

|

Old Section |

New Section |

Nature |

Rate |

Threshold |

|

194H |

393(1) |

Commission/Brokerage |

2% |

₹20,000 |

|

194D |

393(1) |

Insurance Commission |

2% / 10% |

₹20,000 |

🔹 6. Rent & Property Transactions

|

Old Section |

New Section |

Nature |

Rate |

Threshold |

|

194I(a) |

393(1) |

Rent – Machinery |

2% |

₹50K/month |

|

194I(b) |

393(1) |

Rent – Land/Building |

10% |

₹50K/month |

|

194IA |

393(1) |

Property Purchase |

10% |

₹5 lakh |

🔹 7. Investment & Securities Income

|

Old Section |

New Section |

Nature |

Rate |

Threshold |

|

194K |

393(1) |

Mutual Funds |

10% |

₹10,000 |

|

194LBA |

393(1) |

Business Trust |

10% |

NA |

|

194LBB |

393(1) |

Investment Fund |

10% |

NA |

|

194LBC |

393(1) |

Securitisation Trust |

10% |

NA |

|

194 |

393(1) |

Dividend |

10% |

₹10,000 |

🔹 8. Business Transactions & New Age Economy

|

Old Section |

New Section |

Nature |

Rate |

Threshold |

|

194Q |

393(1) |

Purchase of Goods |

0.1% |

₹50 lakh |

|

194O |

393(1) |

E-commerce |

0.1% |

₹5 lakh |

|

194R |

393(1) |

Benefits/Perquisites |

10% |

₹20,000 |

🔹 9. Digital Assets (Crypto, etc.)

|

Old Section |

New Section |

Nature |

Rate |

Threshold |

|

194S |

393(1) |

Virtual Digital Assets |

1% |

₹10,000 |

🔹 10. Insurance & Special Payments

|

Old Section |

New Section |

Nature |

Rate |

Threshold |

|

194DA |

393(1) |

Insurance Payout |

2% |

₹1 lakh |

|

194EE |

393(3) |

NSS Payment |

10% |

₹2,500 |

🔹 11. Winnings & Gambling (Special Category)

|

Old Section |

New Section |

Nature |

Rate |

Threshold |

|

194B |

393(3) |

Lottery/Games |

30% |

₹10,000 |

|

194BA |

393(3) |

Online Gaming |

30% |

₹10,000 |

|

194BB |

393(3) |

Horse Race |

30% |

₹10,000 |

🔹 12. Cash & Partner Payments

|

Old Section |

New Section |

Nature |

Rate |

Threshold |

|

194N |

393(3) |

Cash Withdrawal |

2% |

₹1–3 Cr |

|

194T |

393(3) |

Partner Remuneration |

10% |

₹20,000 |

🔹 13. Foreign Payments (Non-Residents)

|

Old Section |

New Section |

Nature |

Rate |

|

195 |

393(2) |

Foreign Income |

20% / DTAA |

|

194LC |

393(2) |

Foreign Loan Interest |

4% / 5% / 9% |

|

194LD |

393(2) |

Bonds |

5% |

|

196B/C/D |

393(2) |

Securities/GDR |

10% / 12.5% / 20% |

🔹 14. TCS (Tax Collected at Source)

|

Old Section |

New Section |

Nature |

Rate |

|

206C (basic goods) |

394(1) |

Scrap, liquor, etc. |

2% |

|

206C(1F) |

394(1) |

Motor vehicle |

1% |

|

Luxury Goods |

394(1) |

High-value items |

1% |

|

206C(1G) |

394(1) |

Foreign Remittance |

2% / 20% |

|

Tour Packages |

394(1) |

Overseas travel |

2% |

✅ Practical Explanation

🔍 What Actually Changed?

· Section numbers → Changed

· Rates → Same

· Compliance complexity → Increased due to mapping

🧾 Example

A freelancer in Vaishali (201019) receives ₹1,00,000:

· Old Section: 194J

· New Section: 393(1)

· TDS: ₹10,000

A trader in Vasundhra (201012) buys goods worth ₹70 lakh:

· TDS applies on ₹20 lakh

· Rate: 0.1% → ₹2,000

✅ Step-by-Step Compliance

1. Identify payment type

2. Map old section to new section

3. Check threshold

4. Apply rate

5. Deduct & deposit TDS

6. File return using new codes

✅ FAQ

1. Are TDS rates changed in new law?

No, mostly unchanged.

2. Why new sections introduced?

To simplify structure under Income-tax Act 2025.

3. Is section 194J still applicable?

Conceptually yes, but now under section 393(1).

4. What is TDS on crypto?

1% under section 194S.

5. What if PAN not provided?

Higher TDS under section 397(2).

✅ Conclusion

The TDS rate chart FY 2026-27 with section-wise comparison clearly shows that while rates remain same, understanding new section mapping is critical for compliance.

If you are searching for a tax consultant near me, GST services near me, or company registration consultant near me in Ghaziabad (201010), Noida, or Delhi NCR, professional support can help you avoid errors and penalties.

For expert guidance on this topic, contact your tax professional today.

⚠️ Disclaimer

This content is for educational and knowledge purposes only. For verification and applicability to your case, please consult your tax professional.

Have Questions? We're Here to Help

Get expert advice from AMIT SIDDHI AND ASSOCIATES. Reach out to discuss your requirements.