ITR Filing Due Dates & Form Selection for FY 2025-26 (AY 2026-27)

Filing your Income Tax Return (ITR) correctly and on time is essential to avoid penalties and ensure compliance. With updated timelines and form changes, taxpayers must stay informed to prevent costly mistakes.

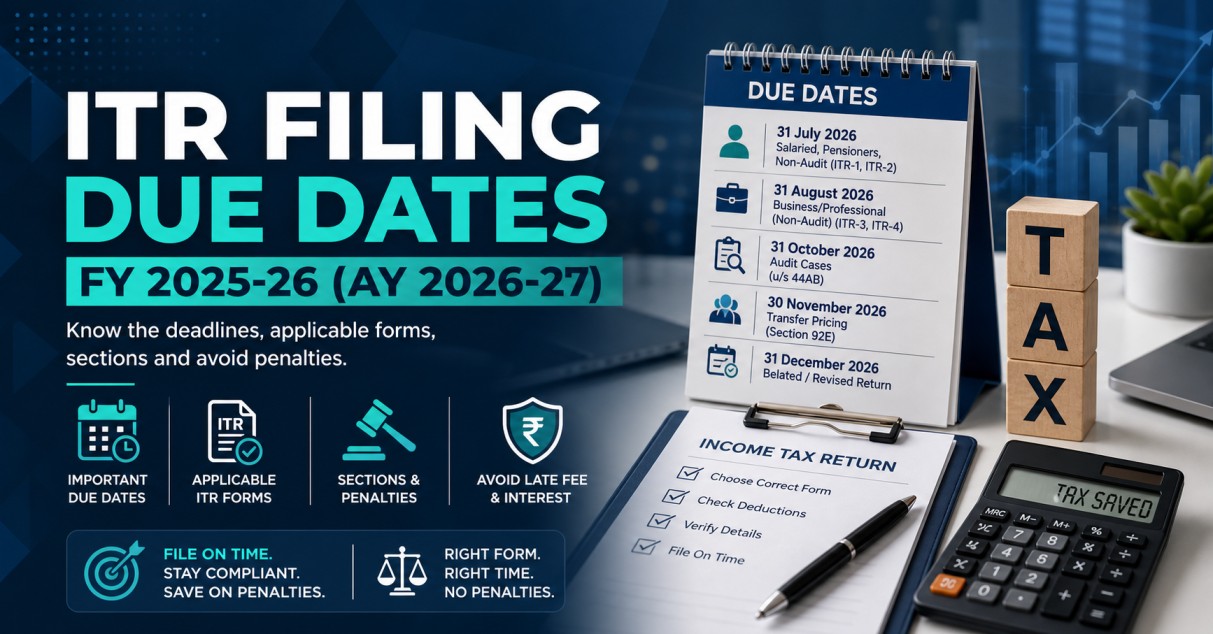

ITR Filing Due Dates for AY 2026-27

The due dates vary depending on the type of taxpayer and audit requirements:

· 31 July 2026

Salaried individuals, pensioners, and non-audit cases filing ITR-1 or ITR-2

· 31 August 2026

Non-audit taxpayers such as freelancers, professionals, and small businesses filing ITR-3 or ITR-4

· 31 October 2026

Taxpayers whose accounts require audit under Section 44AB

· 30 November 2026

Businesses requiring Transfer Pricing Report under Section 92E

· 31 December 2026

Belated or revised return filing deadline

Choosing the Correct ITR Form

Selecting the right form is critical to avoid notices under Section 139(9) (Defective Return).

· ITR-1 (Sahaj)

Applicable for resident individuals with income up to ₹50 lakh from:

• Salary or pension

• One or two house properties (new update)

• Other sources like interest

Not applicable for directors or those holding unlisted shares

· ITR-2

For individuals and HUFs with:

• Capital gains

• Multiple house properties

• Foreign income/assets

• No business income

· ITR-3

For individuals and HUFs having income from business or profession

Suitable for freelancers, consultants, and partners in firms

· ITR-4 (Sugam)

For taxpayers opting for presumptive taxation under Sections 44AD, 44ADA, or 44AE

Applicable if income is up to ₹50 lakh

Now allows reporting up to two house properties

Legal Framework Under Section 139

Understanding different types of returns is crucial:

· Section 139(1) – Original Return

Filed within due date

Mandatory to carry forward business or capital losses

· Section 139(4) – Belated Return

Filed after due date but before 31 December 2026

Loss carry-forward benefit is restricted

· Section 139(5) – Revised Return

Used to correct errors in original or belated return

Updated deadline extended up to 31 March 2027 in certain cases

· Section 139(8A) – Updated Return (ITR-U)

Can be filed within 24 months from end of assessment year

Additional tax of 25% to 50% applicable

Presumptive Taxation Scheme Explained

A simplified taxation option for small taxpayers:

· Section 44AD (Businesses)

• Turnover up to ₹2 crore (₹3 crore if cash receipts ≤ 5%)

• Profit presumed at 6% (digital) or 8% (cash)

· Section 44ADA (Professionals)

• Gross receipts up to ₹50 lakh (₹75 lakh if cash ≤ 5%)

• 50% of receipts treated as profit

Important Note:

If you opt out after choosing presumptive taxation, you cannot re-enter the scheme for 5 years.

Interest and Penalties

Missing deadlines leads to both late fees and interest:

· Section 234F – Late Fee

• ₹5,000 if income exceeds ₹5 lakh

• ₹1,000 if income up to ₹5 lakh

· Section 234A – Delay in Filing

Interest at 1% per month on unpaid tax

· Section 234B – Default in Advance Tax

Applies if less than 90% tax paid

· Section 234C – Deferment of Advance Tax

Interest on missed instalments

Recent Changes for AY 2026-27

· ITR-1 now allows reporting of two house properties

· Mandatory ITR-3 for F&O traders with turnover disclosure

· Political donation claims under Section 80GGC require transaction-level details

Practical Tip / CA Insight

Always reconcile your income with Form 26AS, AIS, and bank statements before filing. Many notices arise due to mismatches. Also, filing before the due date helps avoid interest and allows flexibility for revisions.

FAQ Section

1. Can I file ITR after the due date?

Yes, under Section 139(4), you can file a belated return till 31 December 2026 with late fees.

2. Which ITR form is best for freelancers?

ITR-3 is applicable, or ITR-4 if opting for presumptive taxation under Section 44ADA.

3. What happens if I choose the wrong ITR form?

Your return may be treated as defective under Section 139(9), requiring correction.

4. Can I revise my ITR after filing?

Yes, under Section 139(5), you can revise it within the allowed time.

5. Is it mandatory to pay advance tax?

Yes, if your tax liability exceeds ₹10,000, advance tax provisions apply under Sections 234B and 234C.

Conclusion

Timely and accurate ITR filing is essential to avoid penalties and ensure smooth compliance. Choosing the correct form and understanding applicable sections can save both time and money. Always review your financial data carefully before submission.

For expert guidance on this topic, contact your tax professional today.

Have Questions? We're Here to Help

Get expert advice from AMIT SIDDHI AND ASSOCIATES. Reach out to discuss your requirements.