Form 141 Introduced from April 2026 – Complete Guide to New TDS Filing System

The Income Tax Department has revamped the TDS filing process from April 1, 2026, making compliance simpler yet more structured. If you deal with property, rent, contractors, or crypto transactions, this change directly impacts you.

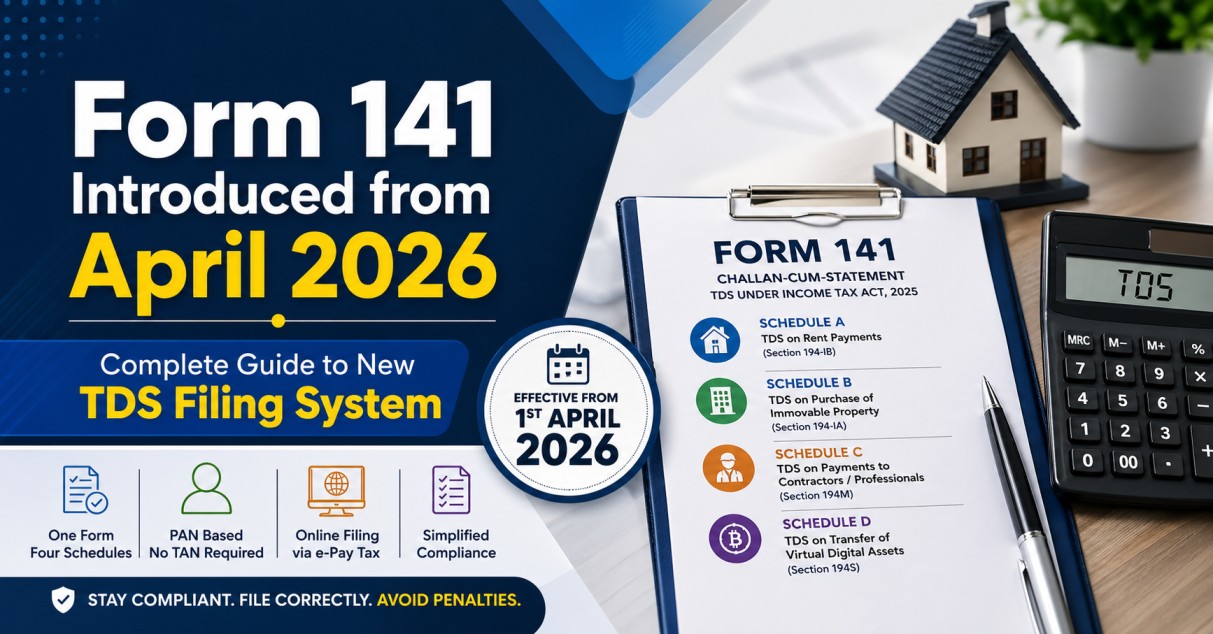

WHAT IS FORM 141?

Form 141 is a new unified challan-cum-statement introduced under the Income Tax Act, 2025. It replaces multiple PAN-based TDS forms into a single, schedule-based system.

Earlier, taxpayers had to choose different forms depending on the nature of the transaction. Now, all such transactions are reported through one form using specific schedules.

OLD VS NEW TDS FORMS

Earlier Forms and Their Replacement:

-

Form 26QB → TDS on property purchase → Now Schedule B in Form 141

-

Form 26QC → TDS on rent (above ₹50,000/month) → Now Schedule A

Need help with this? Talk to AMIT SIDDHI AND ASSOCIATES → -

Form 26QD → TDS on contractor/professional payments → Now Schedule C

-

Form 26QE → TDS on virtual digital assets → Now Schedule D

This consolidation removes confusion and simplifies filing.

KEY FEATURES OF FORM 141

-

Single Form, Multiple Uses

One form with four schedules covers different transaction types. -

PAN-Based Filing

-

No requirement of TAN

-

Applicable mainly to individuals and HUFs

-

-

Online Filing Process

-

Filed through e-Pay Tax section on Income Tax portal

-

Select Form 141 → Choose applicable schedule

-

-

Improved Reporting

-

Better reflection in AIS (Annual Information Statement)

-

Helps avoid mismatches and notices

-

-

Updated TDS Certificates

-

Form 16B replaced by Form 132 (for property transactions)

-

APPLICABLE TRANSACTIONS UNDER FORM 141

Schedule-wise breakdown:

Schedule A

-

TDS on rent payments above ₹50,000/month

-

Covered under Section 194-IB

Schedule B

-

TDS on purchase of immovable property

-

Covered under Section 194-IA

Schedule C

-

TDS on payments to contractors/professionals by individuals/HUFs

-

Covered under Section 194M

Schedule D

-

TDS on transfer of virtual digital assets (crypto, NFTs)

-

Covered under Section 194S

IMPORTANT DEADLINES

-

TDS must be deposited and Form 141 filed within 30 days

from the end of the month in which deduction is made

Example:

If TDS is deducted on April 15, 2026 → Due date will be May 30, 2026

LEGAL REFERENCES (SIMPLIFIED)

Section 194-IA (Property Purchase)

Requires 1% TDS deduction on property transactions exceeding ₹50 lakh.

Section 194-IB (Rent Payments)

Applies to individuals/HUFs paying rent above ₹50,000 per month without needing TAN.

Section 194S (Virtual Digital Assets)

Introduced to bring crypto transactions under tax compliance with TDS provisions.

Income Tax Act, 2025

Introduces structural reforms including unified TDS filing through Form 141.

PRACTICAL EXAMPLE

Case 1: Property Purchase

Mr. A buys a flat in April 2026 for ₹80 lakh.

→ He must file Form 141 using Schedule B

→ Earlier Form 26QB is no longer valid

Case 2: High-Value Rent

Ms. B pays ₹70,000 monthly rent.

→ She must use Schedule A instead of Form 26QC

PRACTICAL TIP / CA INSIGHT

Always determine the date of payment or credit, not agreement date.

If your transaction agreement was signed in March 2026 but payment happens in April 2026:

→ You must use Form 141

→ Using old forms will lead to rejection or compliance notices

Also, ensure correct PAN details of both parties to avoid mismatch in AIS.

FREQUENTLY ASKED QUESTIONS (FAQs)

-

Is TAN required for filing Form 141?

No, Form 141 is PAN-based. TAN is not required for individuals or HUFs. -

What happens if I use old forms after April 1, 2026?

The filing may get rejected or result in non-compliance notices. -

Can multiple buyers/sellers be reported in Form 141?

Yes, the new structure supports multi-party transactions more efficiently. -

What is the penalty for late filing?

Late filing fees under Section 234E and penalties under Section 271H may apply. -

Where can I file Form 141?

It must be filed online through the Income Tax e-filing portal under e-Pay Tax.

CONCLUSION

The introduction of Form 141 is a major step toward simplifying TDS compliance. While the system is more streamlined, taxpayers must be careful about selecting the correct schedule and meeting deadlines to avoid penalties.

For expert guidance on this topic, contact your tax professional today.

Have Questions? We're Here to Help

Get expert advice from AMIT SIDDHI AND ASSOCIATES. Reach out to discuss your requirements.