GST Refund Annexure-B: Meaning, Filing Process, Invoice Matching & Practical Guidance

GST refund filing can become complicated when invoice details do not match portal records or supporting documents are incomplete. One important supporting document in many Input Tax Credit (ITC)-based refund claims is Annexure-B.

Taxpayers in Ghaziabad, Noida, Delhi NCR, and across India frequently face refund delays because inward invoice details are not properly reconciled before filing Form GST RFD-01. Understanding the role of Annexure-B can help reduce notices, deficiency memos, and processing delays.

Whether you are searching for a GST consultant near me, Income tax consultant near me, or GST services near me, knowing how Annexure-B works is essential for smooth refund processing.

Latest Update Section

As per the verified circular material, Annexure-B was modified to include HSN/SAC details for inward invoices wherever applicable.

No recent official update beyond this modification has been verified as of today.

Practical Explanation of Annexure-B

What Exactly Does Annexure-B Contain?

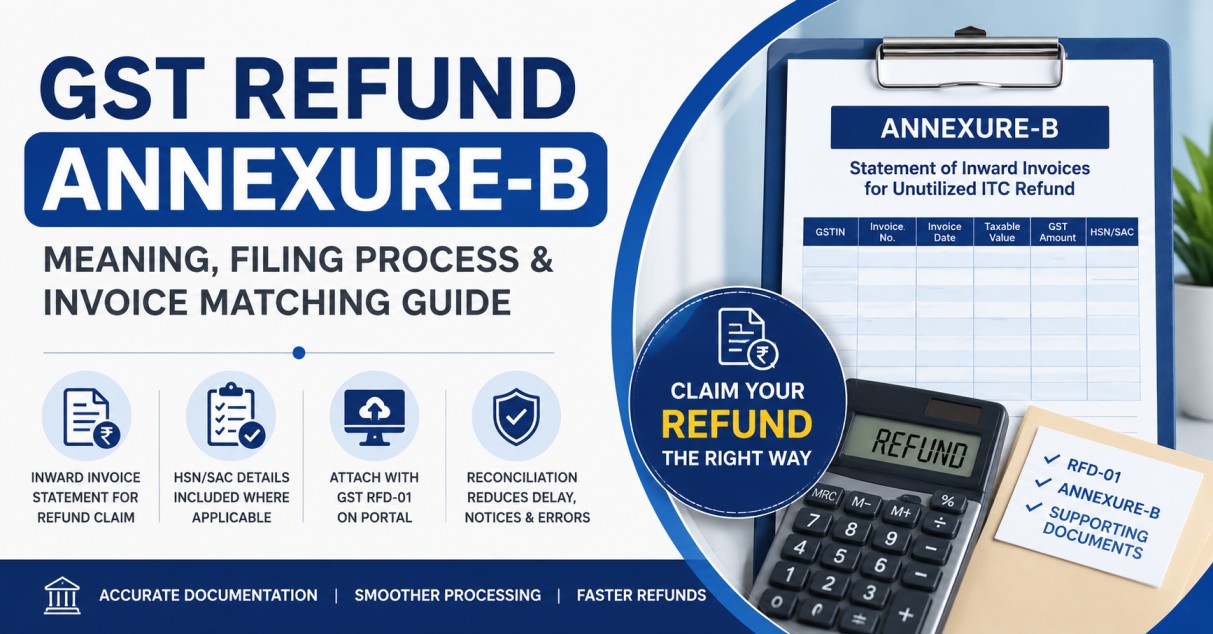

Annexure-B mainly contains inward invoice details linked to Input Tax Credit claimed in a GST refund application. It helps the GST department verify whether the purchases supporting the refund claim are genuine and reflected in GST records.

Typically, the document may include:

| Particular | Purpose |

|---|---|

| Supplier GSTIN | Identification of supplier |

| Invoice Number | Invoice verification |

| Invoice Date | Tax period matching |

| Taxable Value | ITC verification |

| GST Amount | Refund computation |

| HSN/SAC Code | Classification validation |

| GSTR-2A/2B Matching | ITC reconciliation |

Why Is Annexure-B Important?

Many refund applications are delayed because invoice data does not match GST portal records. Annexure-B acts as supporting evidence for the refund claim.

For example:

-

A business exporting goods with payment of tax may claim refund of accumulated ITC.

-

If supplier invoices are missing in GSTR-2B, the department may ask for additional clarification.

-

Proper Annexure-B preparation can reduce refund objections.

Businesses searching for GST consultant near me or GST services near me often require assistance specifically for invoice reconciliation and refund documentation.

Common Refund Types Where Annexure-B May Be Relevant

1. Export Refunds

Used when exporters claim refund of accumulated Input Tax Credit.

2. Inverted Duty Structure Refund

Applicable where input tax rate is higher than output tax rate.

3. Excess Tax Paid Refund

Filed when excess GST was paid accidentally.

4. Accumulated ITC Refund

Used when unutilized ITC accumulates due to business structure or exemptions.

Common Errors in Annexure-B Filing

Invoice Mismatch

The most common issue is mismatch between:

-

Annexure-B

-

GSTR-2A

-

GSTR-2B

-

Supplier filings

Wrong HSN/SAC Details

Since the modified format includes HSN/SAC details wherever applicable, incorrect classification can trigger scrutiny.

Duplicate Invoice Entries

Duplicate upload of invoices can result in portal validation errors.

Incorrect Refund Category

Selecting the wrong refund category in RFD-01 may lead to rejection or deficiency memo.

Unsupported ITC Claim

Claiming ITC without valid invoice support can delay processing.

Step-by-Step GST Refund Filing Process with Annexure-B

Step 1 – Identify Refund Category

Determine whether the refund relates to:

-

Export

-

Accumulated ITC

-

Excess tax payment

-

Inverted duty structure

Step 2 – Reconcile Purchase Data

Match:

-

Purchase register

-

GSTR-2A

-

GSTR-2B

-

Vendor invoices

This is one of the most important compliance steps.

Step 3 – Prepare Annexure-B

Compile inward invoice details carefully.

Ensure:

-

GSTIN is correct

-

Invoice numbers match

-

Tax amounts are accurate

-

HSN/SAC details are included wherever applicable

Step 4 – File Form GST RFD-01

Upload the refund application through the GST portal along with supporting documents.

Step 5 – Validate Uploaded Data

The GST portal may reject or flag files if formatting or invoice details are incorrect.

Step 6 – Department Verification

The tax officer may:

-

Approve refund

-

Seek clarification

-

Issue deficiency memo

-

Request additional records

Step 7 – Refund Processing

After verification, eligible refund amount is processed.

Practical Tips Before Filing GST Refund

Maintain Proper Vendor Reconciliation

Ensure suppliers file GSTR-1 correctly and on time.

Review HSN/SAC Carefully

Incorrect HSN/SAC classification can create unnecessary scrutiny.

Keep Supporting Documents Ready

Maintain:

-

Tax invoices

-

Purchase register

-

Shipping documents (if exports involved)

-

LUT/Bond documents

-

Bank realization records where applicable

Avoid Last-Minute Filing

Late reconciliation increases chances of mismatch and notices.

Businesses in Vaishali (201019), Indirapuram (201014), Vasundhra (201012), and nearby NCR areas frequently seek professional help for GST refund reconciliation due to increasing scrutiny on ITC claims.

FAQ

1. Is Annexure-B a separate GST refund form?

No. Annexure-B is not a standalone refund form. It is a supporting statement attached with refund applications involving unutilized ITC.

2. Is Annexure-B mandatory for all GST refunds?

The requirement depends on the refund category and portal/document requirements applicable to the claim.

3. Does Annexure-B include HSN/SAC details?

Yes, the verified material confirms that the modified format includes HSN/SAC details wherever applicable.

4. Is JSON upload compulsory for Annexure-B?

The verified material does not confirm a universal mandatory rule requiring all refund applicants to upload Annexure-B through JSON format separately.

5. What happens if invoice details do not match?

The portal or tax officer may issue errors, notices, or deficiency memos if invoice details are inconsistent.

6. Can missing GSTR-2B invoices still be reported?

Where invoices are not auto-populated, applicants may need to provide details in Annexure-B as supporting records.

LEGAL POSITION

Legal Reference

Relevant provisions and refund procedures generally relate to GST refund filing under Form GST RFD-01 and supporting documentation requirements prescribed under GST law and portal procedures.

Official GST Portal:

https://www.gst.gov.in/

CBIC Official Website:

https://cbic-gst.gov.in/

Verified Content

Annexure-B is the statement of inward invoices submitted with a refund application for unutilized ITC. The verified circular material says it was modified to include HSN/SAC details for inward invoices where applicable.

It is not a standalone refund form; it is a supporting document attached to the refund application.

Prepare the refund category and confirm eligibility, such as export refund, accumulated ITC refund, excess tax paid, or inverted duty structure refund.

File Form GST RFD-01 on the GST portal with the required supporting documents.

Attach the invoice statement as Annexure-B where required, including HSN/SAC details if applicable under the modified format.

The portal validates the uploaded data and may return errors if the format or details are incorrect.

After submission, the tax officer may examine the claim and process the refund or issue deficiency/notice if documents or data do not match.

The safest approach is to reconcile the refund claim with inward invoices and supporting GST data before filing. Annexure-B is meant to help tax authorities verify the legitimacy of the refund claim against actual purchases.

For ITC-based refunds, keep the invoice details, GSTR-2A/GSTR-2B matching, and HSN/SAC details ready wherever relevant.

If an invoice is not reflected in the auto-populated statement, the applicant may need to provide the details in Annexure-B as part of the supporting records.

The verified material supports that GST portal uploads can involve JSON files in some return-related workflows, but it does not verify a universal official rule that every refund applicant must separately upload Annexure-B in JSON format through an offline utility.

So, the claim should be treated cautiously as a portal/process update unless the exact GST advisory or circular is produced from an official source.

If you are filing a refund, the practical process is: identify the refund type, prepare RFD-01, compile the supporting invoices, complete Annexure-B if required, reconcile it with your GST records, and submit through the portal with correct format and backup documents.

This reduces the chance of deficiency memo, notice, or delay.

Conclusion

Annexure-B plays an important role in GST refund processing by helping authorities verify inward invoices supporting the refund claim. Proper reconciliation of invoices, GSTR-2A/2B matching, and accurate HSN/SAC reporting can significantly reduce refund delays and notices.

If you are looking for GST services near me, Tax consultant near me, Company registration consultant near me, or Income tax services near me, professional reconciliation and documentation support can help ensure smoother refund processing.

For expert guidance on this topic, contact your tax professional today.

FINAL DISCLAIMER

This content is for educational and knowledge purposes only. For verification and applicability to your case, please consult your tax professional.

Have Questions? We're Here to Help

Get expert advice from AMIT SIDDHI AND ASSOCIATES. Reach out to discuss your requirements.