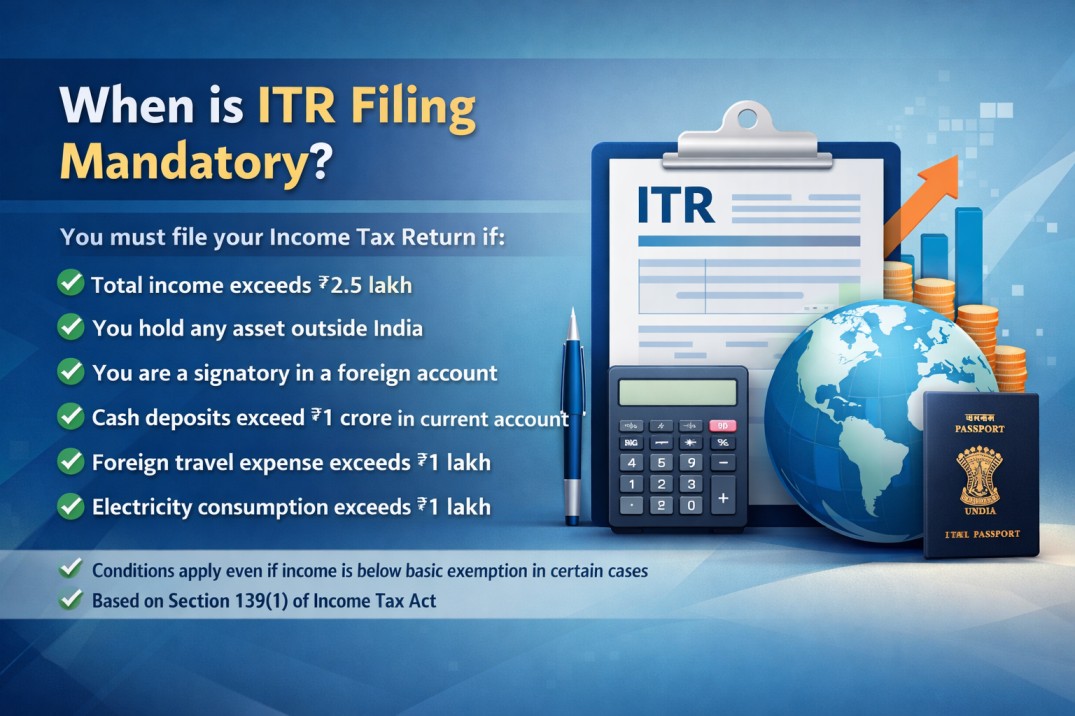

WHEN IS ITR FILING MANDATORY IN INDIA?

Many taxpayers assume that Income Tax Return (ITR) filing is required only when income exceeds the basic exemption limit. However, under Indian tax laws, there are several situations where filing becomes mandatory even if income is low.

When is ITR Filing Mandatory?

As per Section 139(1) of the Income Tax Act, filing of ITR is compulsory in the following cases:

- Income Exceeds Basic Exemption Limit

- If your total income exceeds ₹2.5 lakh (for individuals below 60 years), you must file ITR.

- For senior citizens, limits differ, but filing is still mandatory if crossed.

- Ownership of Foreign Assets

- If you hold any asset outside India (bank account, property, shares, etc.), ITR filing is mandatory.

- Even if there is no income from such assets, disclosure is required.

- Signatory in Foreign Account

- If you are an authorized signatory in any foreign bank account, you must file ITR.

- High-Value Financial Transactions

ITR filing becomes mandatory if you have undertaken certain high-value transactions:

- Cash deposits exceeding ₹1 crore in one or more current accounts

- Foreign travel expenses exceeding ₹2 lakh in a financial year

- Electricity consumption exceeding ₹1 lakh annually

These conditions apply regardless of your income level.

- Business or Professional Income (Presumptive Cases)

- If you opt out of presumptive taxation under Section 44AD or 44ADA and your income exceeds the basic exemption limit, filing becomes compulsory.

- TDS or TCS Deduction

- If TDS/TCS is deducted and you wish to claim a refund, filing ITR is necessary.

Important Legal References

- Section 139(1): Specifies mandatory filing conditions and due dates

- Rule 12AB of Income Tax Rules: Prescribes ITR forms and disclosure requirements

- CBDT Notification No. 37/2022: Introduced conditions for mandatory filing based on high-value transactions

These provisions ensure transparency and widen the tax base.

Real-Life Example

Mr. A has income of ₹2.2 lakh (below exemption limit), but he spent ₹3 lakh on foreign travel during the year.

Even though his income is not taxable, he must file ITR due to high-value transaction rules.

Practical Tip / CA Insight

- Do not assume that low income means no compliance

- Always review your financial transactions during the year

- Filing ITR helps in:

• Loan approvals

• Visa applications

• Claiming refunds

• Avoiding notices from the Income Tax Department

FAQ Section

- Is ITR filing mandatory if income is below ₹2.5 lakh?

Yes, if you meet conditions like foreign assets, high-value transactions, or signatory authority in foreign accounts. - What happens if I don’t file ITR when required?

You may face penalties under Section 234F, interest, and possible notices from the department. - Is electricity consumption really a criterion?

Yes, if your electricity bills exceed ₹1 lakh annually, ITR filing becomes mandatory. - Do students need to file ITR?

Only if they meet any of the mandatory conditions or want to claim a refund. - Can I file ITR voluntarily?

Yes, even if not mandatory, voluntary filing is beneficial for financial records and future compliance.

Conclusion

ITR filing is not just about income—it also depends on your financial activities. Ignoring mandatory filing conditions can lead to penalties and scrutiny. Always evaluate your transactions and comply timely to stay on the safe side.

For expert guidance on this topic, contact your tax professional today.

Have Questions? We're Here to Help

Get expert advice from AMIT SIDDHI AND ASSOCIATES. Reach out to discuss your requirements.