Income Tax Penalty Increased to ₹25,000 for Non-Compliance During Tax Inspections

Many businesses, professionals, startups, and traders are unaware that the Income-tax compliance framework applicable from 1 April 2026 has significantly increased the penalty for failing to provide business or professional information when requested by tax authorities during inspections.

If you are searching in Ghaziabad, Noida, Indirapuram, Vaishali, Vasundhara, Delhi NCR, or nearby areas for an Income tax consultant near me, GST consultant near me, or tax consultant near me to understand inspection-related compliance under the Income-tax Act, 2025, this amendment is important for your business operations and recordkeeping practices.

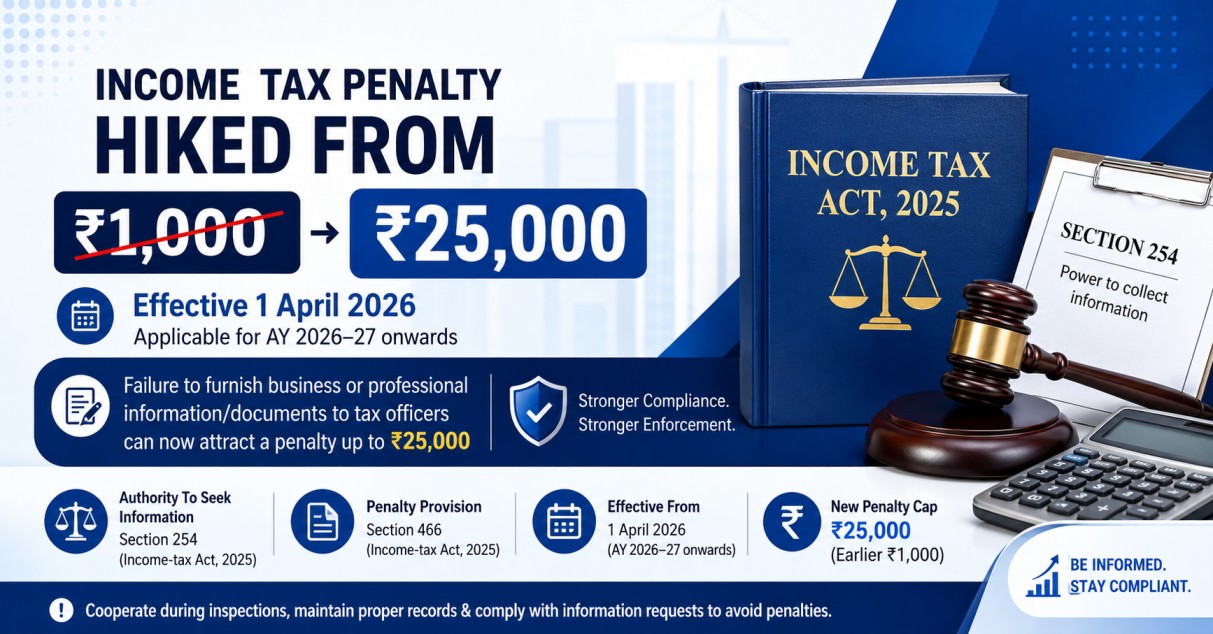

The Finance Bill 2026 framework has raised the maximum penalty from ₹1,000 to ₹25,000 where a taxpayer refuses or fails to furnish required information or documents during inspection proceedings conducted by income-tax authorities. The amendment applies from 1 April 2026 onward for tax year 2026–27 and subsequent years.

Latest Update

The Finance Bill 2026 / Income-tax Act, 2025 framework increased the penalty cap for non-compliance with information requests made by income-tax authorities during inspections or visits.

Key update:

- Earlier penalty cap: ₹1,000

- Revised penalty cap: ₹25,000

- Effective date: 1 April 2026

- Applicable from: AY 2026–27 onward

- Information gathering authority continues under Section 254

- Penalty amendment reflected in Section 466 under the new framework

No recent official update beyond the notified 2026 framework has been found as of today.

Practical Explanation for Businesses and Professionals

Why This Amendment Matters

Earlier, the penalty of ₹1,000 was considered too small to act as a deterrent for non-cooperation during tax inspections. For medium and large businesses, such penalties often had negligible impact.

The government has now increased the penalty ceiling to ₹25,000 to strengthen compliance and ensure taxpayers cooperate during official inspection proceedings.

This change especially affects:

- Traders

- Professionals

- MSMEs

- Startups

- Companies

- Partnership firms

- Consultants

- Service providers

- Freelancers maintaining books of account

Businesses located in Ghaziabad (201010), Noida, Indirapuram (201014), Vaishali (201019), and other Delhi NCR areas should ensure their accounting and documentation systems are properly maintained because inspection proceedings may now carry higher financial exposure for non-compliance.

Comparison Table – Earlier vs Revised Penalty

|

Particulars |

Earlier Provision |

Revised Provision |

|

Maximum penalty for failure to furnish information |

₹1,000 |

₹25,000 |

|

Applicable authority |

Income-tax authority |

Income-tax authority |

|

Relevant inspection power |

Section 254 |

Section 254 |

|

Effective date |

Earlier framework |

1 April 2026 |

|

Applicable AY |

Previous years |

AY 2026–27 onward |

Real-Life Practical Example

Suppose an authorised income-tax officer visits a business premises during inspection proceedings and requests:

- Purchase invoices

- Cash book

- Sales records

- Ledger copies

- GST reconciliation data

- Digital accounting backup

If the taxpayer intentionally refuses to provide records or delays compliance without reasonable cause, the officer may initiate penalty proceedings under the revised framework.

Earlier, the maximum exposure was only ₹1,000. Under the new framework effective from 1 April 2026, the penalty can now extend up to ₹25,000.

This makes proper bookkeeping and prompt response during inspections far more important for businesses and professionals.

What Businesses Should Do Now

1. Maintain Proper Books of Account

Businesses should ensure:

- Updated accounting records

- Proper invoice management

- Bank reconciliation

- GST reconciliation

- Digital backup systems

- Proper documentation retention

Well-organised records reduce disputes during inspections.

2. Cooperate During Inspections

When authorised officers request documents:

- Respond professionally

- Provide available records promptly

- Avoid unnecessary delays

- Maintain written communication records

- Seek professional advice immediately if required

3. Digitise Compliance Records

Digital bookkeeping systems can significantly reduce compliance risk.

Businesses using:

- Cloud accounting

- ERP systems

- Digital invoice archives

- Proper GST reconciliation tools

will generally find inspection handling easier and faster.

4. Consult Tax Professionals Immediately

If you receive:

- Inspection notice

- Information request

- Show-cause notice

- Penalty communication

you should immediately consult a tax professional.

Many businesses searching for Income tax services near me, GST services near me, or tax consultant near me in Noida, Vasundhara (201012), Ghaziabad, and Delhi NCR usually require immediate guidance during inspection or penalty proceedings.

What This Amendment Does NOT Mean

No New Return Filing

The amendment does not introduce:

- New ITR forms

- Separate inspection return

- Additional compliance portal filing

- New annual statement

It only increases the penalty limit for non-compliance during information requests.

No Unlimited Search Powers

The amendment does not give unlimited authority to tax officers.

Inspection powers remain governed by:

- Section 254

- Statutory safeguards

- Legal procedures

- Constitutional protections

Authorities must still follow due process.

Step-by-Step Compliance Process During Tax Inspection

Step 1 — Verify Officer Authorization

Check identity and authorization of the officer conducting inspection proceedings.

Step 2 — Understand Information Requested

Review the documents or records requested carefully.

Step 3 — Produce Available Records

Provide relevant books, invoices, or digital data wherever lawfully required.

Step 4 — Keep Communication Records

Maintain copies of notices, replies, emails, and acknowledgements.

Step 5 — Seek Professional Guidance

Consult your tax professional before refusing or delaying any request.

Step 6 — Respond to Show-Cause Notices

If penalty proceedings are initiated, submit proper written explanations within timelines.

Step 7 — Consider Appeal Rights

Where penalty orders are passed, statutory appeal remedies may be available under the Act.

Legal Reference

Section

Power to collect information — Section 254 (Income-tax Act, 2025)

Rule

Not applicable (statutory amendment in the Act)

Notification / Circular

Income-tax Rules, 2026 brought into force from 1 April 2026

Official Source Links

https://www.incometaxindia.gov.in/documents/d/guest/en-notified-it-rules-2026-20-03-2026-pdf

Legal Position

The restructured Income-tax Act (titled Income-tax Act, 2025) separates the authority to seek information and the penalty for non-compliance. Section 254 under the new numbering sets out powers for officers to require information at business or professional premises, while the penalty provision that penalises failure to comply has been amended to increase the maximum monetary penalty from ₹1,000 to ₹25,000 by substituting the figure in the relevant penalty section, referred to in published summaries as Section 466.

The amendment takes effect from 1 April 2026 and applies for tax year 2026–27 and subsequent years.

This is not a new return filing requirement or a new form introduction. The amendment simply increases the maximum monetary penalty that may be imposed where a taxpayer refuses or fails to furnish documents, records, books of account, or information required during inspection proceedings.

The enhanced penalty applies where a person fails to provide information or documentation requested by income-tax authorities under statutory powers during inspections or visits conducted under Section 254.

The enforcement of the penalty remains subject to statutory procedures, legal safeguards, and limits prescribed under the Act and applicable rules.

YES — The claim is verified. The penalty cap for failure to provide business or professional information to tax officers has been increased from ₹1,000 to ₹25,000 effective from 1 April 2026 under the Income-tax Act, 2025 / Finance Bill 2026 framework.

Frequently Asked Questions (FAQs)

1. What is the revised penalty amount under the new Income-tax framework?

The maximum penalty has been increased from ₹1,000 to ₹25,000 effective from 1 April 2026.

2. Which section gives tax officers power to seek information?

The information gathering authority continues under Section 254 of the Income-tax Act, 2025.

3. Is any new return filing required because of this amendment?

No. The amendment only increases the penalty cap for non-compliance during inspections.

4. From when is the revised penalty applicable?

The revised penalty applies from 1 April 2026 for AY 2026–27 onward.

5. Can the penalty be challenged?

Yes. Taxpayers may have legal remedies including explanation submissions and statutory appeals depending on facts and procedure.

6. Why should businesses maintain digital records now?

Digital records help businesses quickly respond to inspection-related information requests and reduce compliance disputes.

7. Should small businesses also worry about this amendment?

Yes. The provision can apply to businesses and professionals of different sizes if they fail to furnish requested information during inspection proceedings.

Conclusion

The increase in penalty from ₹1,000 to ₹25,000 marks a significant compliance shift under the Income-tax Act, 2025 framework. Businesses and professionals should not treat inspection-related information requests casually after 1 April 2026.

Strong bookkeeping systems, digital record management, timely cooperation, and professional guidance are now more important than ever to avoid unnecessary penalty exposure.

If you are searching for an Income tax consultant near me, GST consultant near me, Company registration consultant near me, Trade Mark consultant near me, logo registration consultant near me, or professional tax compliance assistance in Ghaziabad, Noida, Indirapuram, Vaishali, Vasundhara, and Delhi NCR, timely professional support can help reduce litigation and compliance risks.

For expert guidance on this topic, contact your tax professional today.

Final Disclaimer

This content is for educational and knowledge purposes only. For verification and applicability to your case, please consult your tax professional.

Have Questions? We're Here to Help

Get expert advice from AMIT SIDDHI AND ASSOCIATES. Reach out to discuss your requirements.