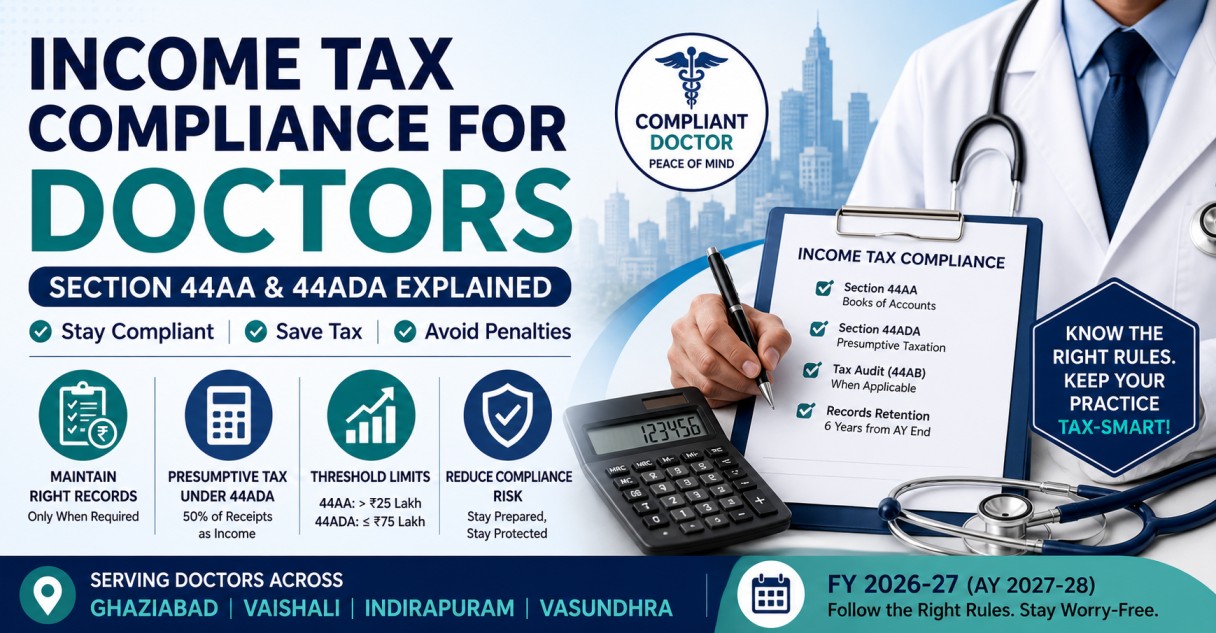

Income Tax Compliance for Doctors – Section 44AA & 44ADA Explained

Income tax compliance for doctors is often misunderstood due to myths around record-keeping and taxation rules. If you are a practicing doctor in Ghaziabad, Vaishali, or Indirapuram, understanding Section 44AA and Section 44ADA is essential to avoid penalties and unnecessary compliance burden.

This guide explains the correct legal position as per Income Tax Act, 1961 and Rules, 1962 (updated till FY 2026–27).

Legal Framework for Doctors

Doctors fall under “specified professions” as per the Income Tax Act.

Applicable Sections:

- Section 44AA(1) – Maintenance of Books (specifically includes doctors)

- Section 44ADA – Presumptive taxation for professionals

- Section 44AB – Tax audit

As per the official portal (https://incometax.gov.in), there is no requirement for any Form 25 or daily patient register under tax laws.

Section 44AA – When Books of Accounts Are Mandatory

Books must be maintained if:

- Gross receipts exceed ₹25 lakh in any of the last 3 financial years, OR

- Income exceeds ₹2.5 lakh

Required Records (Rule 6F):

- Cash book

- Ledger

- Bills and receipts

- Expense vouchers

- Daily cash balance

Important Clarification:

- There is no requirement to maintain patient-wise daily entries

- Focus is on financial records, not clinical logs

Section 44ADA – Presumptive Taxation for Doctors

This is the most practical option for many professionals.

Key Conditions:

- Gross receipts ≤ ₹75 lakh

- Cash receipts ≤ 5% (i.e., 95%+ digital transactions preferred)

- 50% of receipts treated as taxable income

Benefits:

- No need to maintain detailed books

- No audit required (if 50% income declared)

- Simplified compliance

Example:

A doctor in Indirapuram (201014) earns ₹50 lakh:

- Declares ₹25 lakh as income

- No books or audit required

Important Note:

If you:

- Declare income less than 50%, then:

- Books of accounts become mandatory

- Tax audit under Section 44AB applies

Do Doctors Need Daily Patient Records?

Legal Position:

- No mandatory requirement under Income Tax law

- No prescribed format like daily case register

Practical Recommendation:

Maintain basic tracking such as:

- Daily receipt summary

- Digital payment reports

- Billing records

This helps during:

- Scrutiny

- Loan applications

- Financial planning

Digital Record Keeping – Updated Compliance View

Digital systems are fully valid and widely used.

Best Practices:

- Use accounting or clinic software

- Maintain proper audit trail

- Ensure data consistency with bank records

- Take regular backups

Important:

CBDT guidance allows digital books, but:

- Records must be reliable and verifiable

- No requirement for real-time AI reporting or India-only servers

Tax Audit – Section 44AB

When Audit Applies:

| Scenario | Condition |

|---|---|

| Not opting 44ADA | Receipts exceed ₹75 lakh |

| Opting 44ADA but declaring <50% income | Audit required |

Record Preservation – Rule 6F

- Maintain records for 6 years from end of relevant Assessment Year

Example:

- FY 2026–27 → AY 2027–28

- Preserve till end of AY 2033–34

Comparison – Section 44AA vs 44ADA

| Particulars | Section 44AA | Section 44ADA |

|---|---|---|

| Books required | Yes | No (if 50% income declared) |

| Audit | Possible | Not required |

| Compliance burden | High | Low |

| Ideal for | Large clinics | Small/medium doctors |

Practical CA Insight

- If your receipts are below ₹75 lakh → opt 44ADA wherever possible

- Maintain basic receipt tracking even under presumptive scheme

- Ensure:

- Bank deposits match declared income

- UPI/cash records are consistent

If you are searching for a CA in Ghaziabad or tax consultant near me, proper structuring can reduce both tax and compliance stress.

Common Mistakes to Avoid

- Following non-existent formats like “Form 25”

- Over-maintaining unnecessary registers

- Ignoring 44ADA benefits

- Declaring low income without audit

- Not reconciling bank transactions

FAQ – Income Tax for Doctors

1. Is there any Form 25 for doctors?

No, it does not exist under Income Tax Act or Rules.

2. Are doctors required to maintain patient-wise records?

No, not under tax law.

3. What is the limit for maintaining books?

₹25 lakh gross receipts under Section 44AA.

4. Can doctors opt for presumptive taxation?

Yes, under Section 44ADA if receipts ≤ ₹75 lakh.

5. Is digital accounting allowed?

Yes, provided proper audit trail is maintained.

6. How long should records be preserved?

6 years from end of relevant assessment year.

Conclusion

Income tax compliance for doctors should always be based on actual law, not assumptions or viral content. Sections 44AA and 44ADA provide a clear and practical framework for compliance.

Doctors practicing in Vaishali, Indirapuram, or across Ghaziabad can significantly reduce compliance burden by choosing the right taxation method and maintaining proper financial discipline.

For expert guidance on this topic, contact your tax professional today.

Have Questions? We're Here to Help

Get expert advice from AMIT SIDDHI AND ASSOCIATES. Reach out to discuss your requirements.