Calcutta High Court Rules: GST Refund Filed Within Two Years Cannot Be Denied Based on Later Circular

Calcutta High Court Rules: GST Refund Filed Within Two Years Cannot Be Denied Based on Later Circular

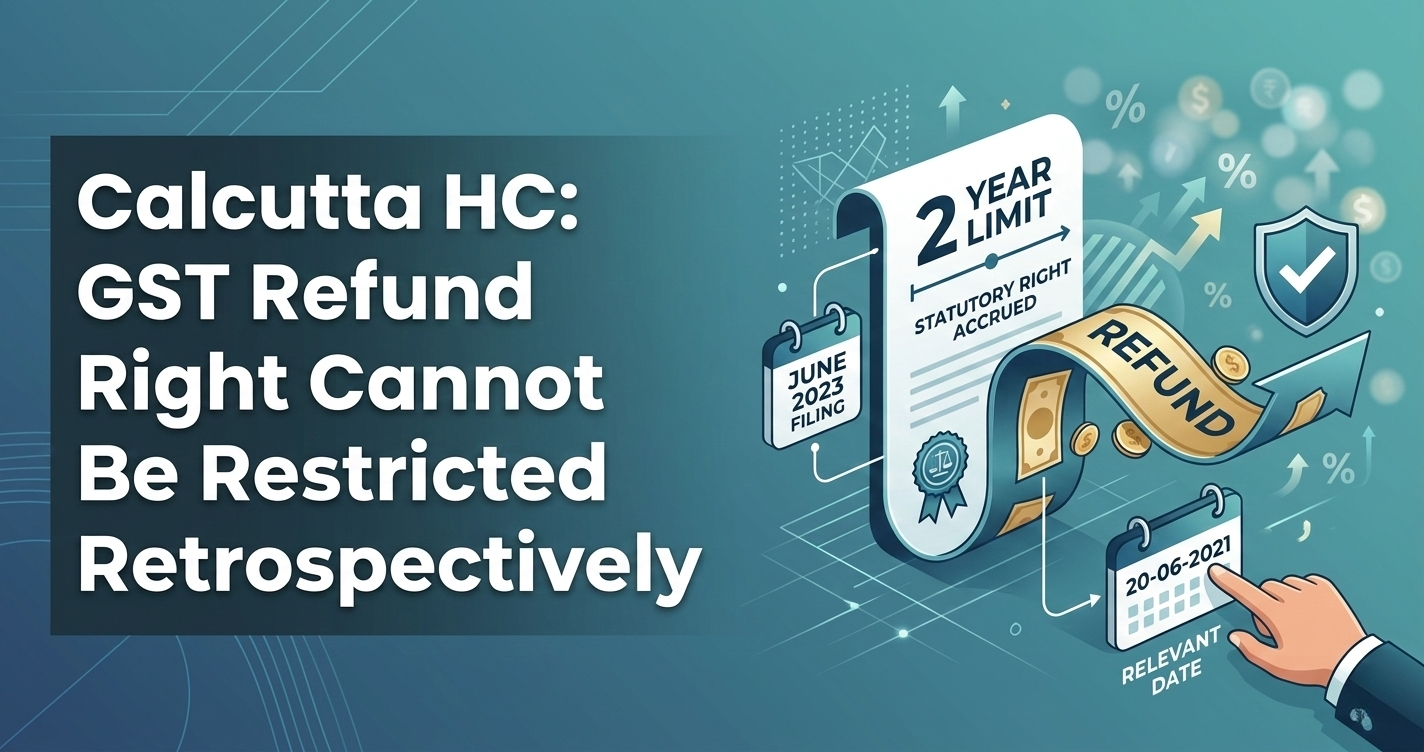

In a significant ruling, Adani Wilmer Ltd. v. Assistant Commissioner of State Tax, the Calcutta High Court has clarified the hierarchy of statutory rights over executive circulars in GST refund claims. The court held that a legitimate refund claim filed within the prescribed statutory timeline cannot be curtailed retrospectively by a circular issued after the right to claim the refund has already accrued.

Background of the Case

The assessee, Adani Wilmer Ltd., filed an application in June 2023 for a refund of accumulated unutilized ITC for the tax period of May 2021. This claim arose from an inverted duty structure. The application was filed within the two-year limitation period stipulated under Section 54(1) of the CGST Act, 2017, calculated from the relevant date (the due date of the return, which was 20-06-2021).

However, the proper officer rejected the refund application. The rejection was based solely on CBIC Circular No. 181/13/2022-GST, which stated that certain restrictions on such refunds would apply to applications filed on or after 18-07-2022.

The Calcutta High Court’s Decision

The High Court sets aside the rejection orders, establishing the following legal positions:

-

Statutory Right Prevails: The court ruled that an executive circular cannot retrospectively restrict or curtail a statutory right to claim a refund once that right has accrued.

-

Timely Filing: It was confirmed that the relevant date for the refund was 20-06-2021, and the application filed in June 2023 was well within the two-year limit prescribed u/s 54(1).

Need help with this? Talk to AMIT SIDDHI AND ASSOCIATES → -

Circular Inapplicable: The authority was directed to reconsider the refund claim purely on its merits, ignoring the restrictive conditions of Circular No. 181/13/2022-GST.

Legal Significance

This judgment is a crucial precedent for taxpayers facing refund rejections based on retrospective circular interpretations. It reinforces the principle that circulars are meant to clarify and explain the law, not to override or change the substantive rights granted by the parent statute (the GST Act).

Regulatory Reference

-

Section 54(1), CGST Act, 2017: Pertaining to Refunds of Tax.

Need help with this? Talk to AMIT SIDDHI AND ASSOCIATES → -

CBIC Circular No. 181/13/2022-GST: Clarification regarding refund of unutilized ITC on inverted duty structure.

-

Adani Wilmer Ltd. v. Assistant Commissioner of State Tax (WPA No. 27066 of 2024).

For expert guidance on this topic, contact your tax professional today.

Have Questions? We're Here to Help

Get expert advice from AMIT SIDDHI AND ASSOCIATES. Reach out to discuss your requirements.